The three commonly used formula for Office Overhead Claims

Theme: Project Closure, Module: Claims & Disputes

Author: Dr. Pradeep Reddy Sarvareddy

Published Date: 10 July 2026

Whenever a project is delayed Contractors raise several Claims, including claims related to idle machinery, extended labour, security, watchman salaries, etc, and the Office overhead Claim. The head office overheads include Rent, salaries of the Contractor’s engineers and accountants, admin staff, Contractor’s own time, etc. If a Contractor is working on 10 different projects, obviously the head office overheads are proportionately accounted for each project.

Over the years, three methods have become the standard ones used in construction disputes in India: Hudson's formula, Emden's formula and Eichleay's formula. Each is simply a different, structured way of answering the same question, i.e., given the delay, what did it actually cost the head office for this project? These formula differ in where they get their numbers from.

One very critical information. This article is about office overheads, but none of these three formulae actually confine themselves to overheads alone. All three formula, in their standard form, bundle “overheads + profit” into a single percentage or a single computation. Courts, when they discuss these formulae, usually call the resulting claim "loss of profit" rather than "loss of overheads," even though a large part of what's being recovered is the Contractor's office running cost. So if you come across judgments discussing Hudson's, Emden's or Eichleay's under the heading of "loss of profit", don't assume they are talking about something different from what this article covers, as they are very often talking about the same claim, just under a different name. One word of advice would be to use the formula and then separate out the profit or change your claim as “overheads + profit”.

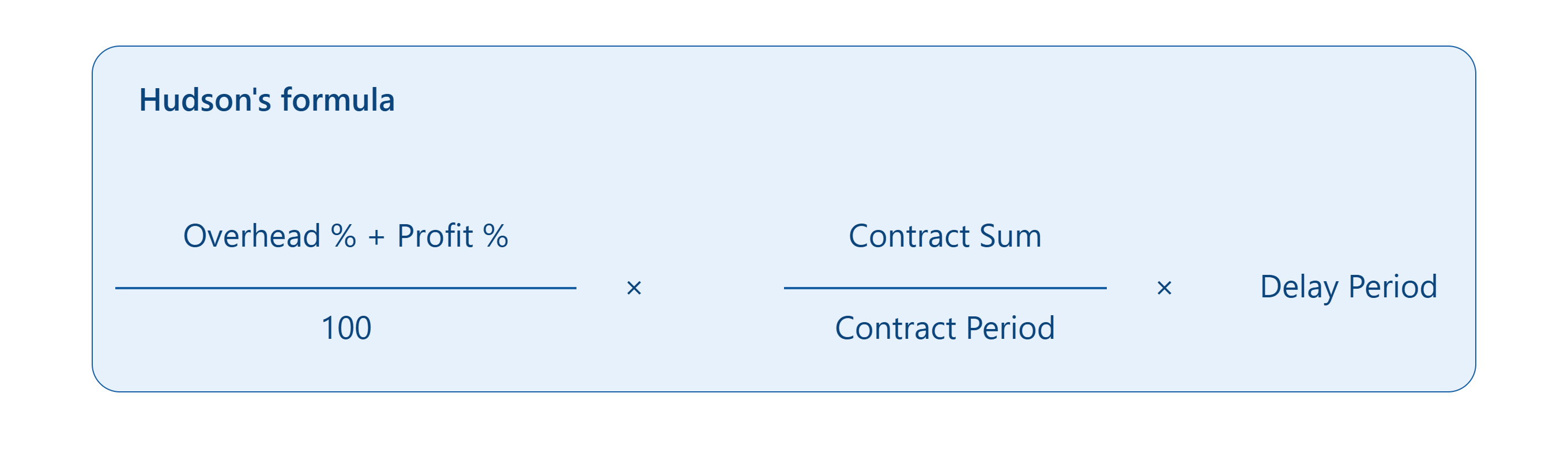

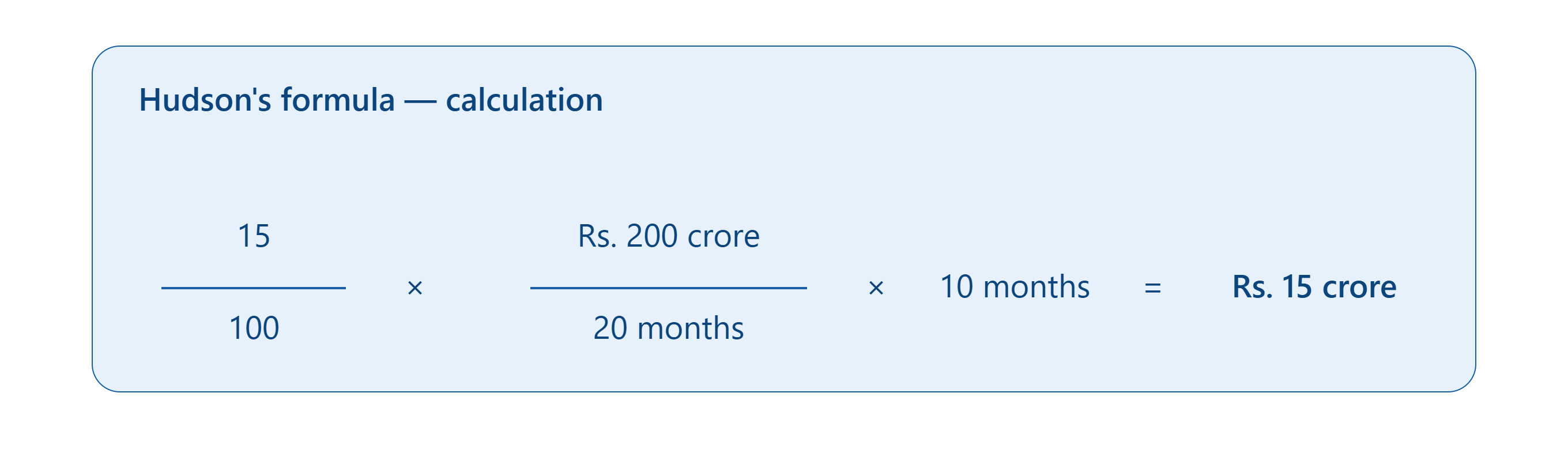

Hudson's formula uses the figures the Contractor himself worked into the bid at the time of tendering. When a Contractor bid for a project, the Contractor would obviously include a cost for the office running costs and profit. This method goes back to that original pricing and adjusts it across the extra time the project was delayed. The formula is most sought out (and also the most criticised) because it is simple and it uses the Contractor’s own numbers, and a Contractor cannot easily be blamed as having invented the figure, because it was there in the tender from day one. This formula is criticised exactly for the same reasons: it assumes the tender pricing was accurate and realistic, which the Department will always dispute.

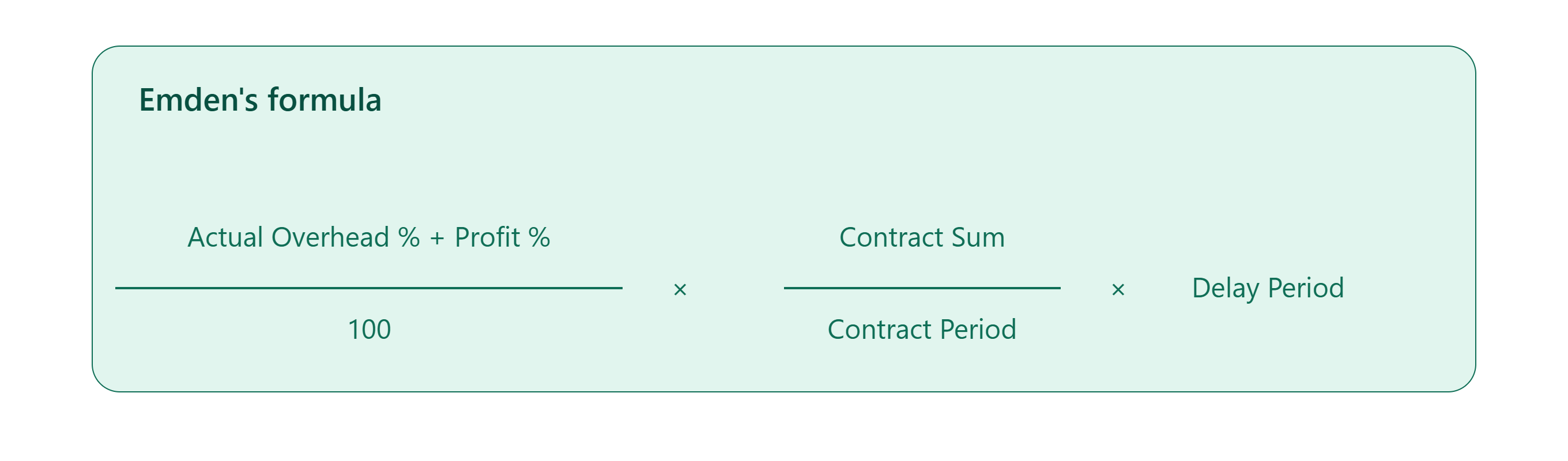

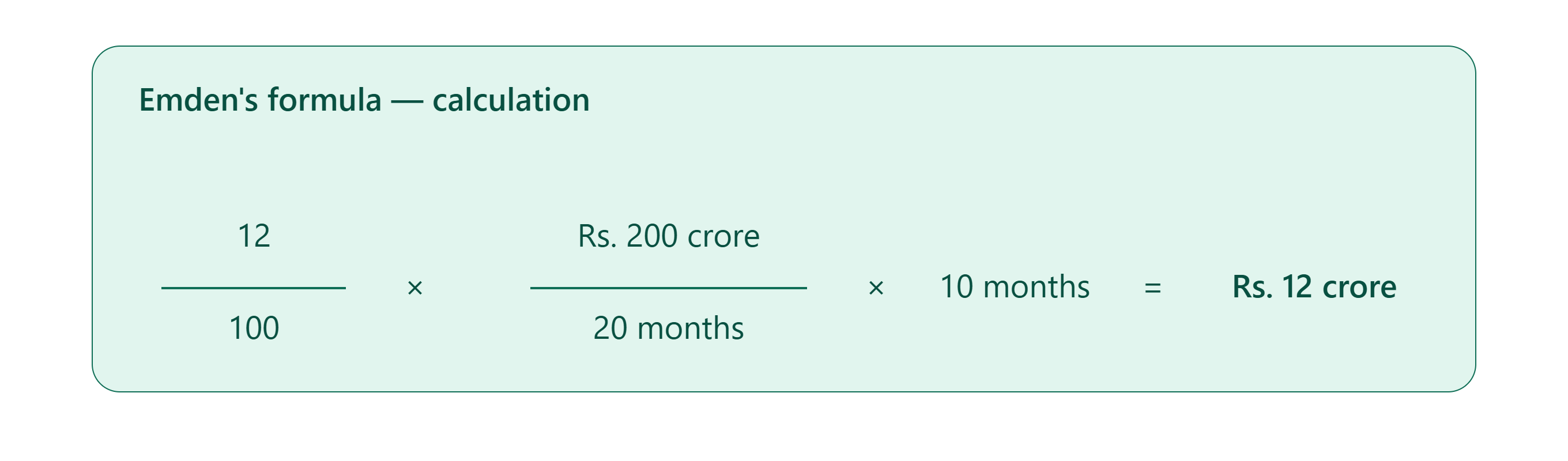

Emden's formula doesn't look at what the Contractor bid for this one project. It looks at the company as a whole, i.e., the actual, audited overhead costs across the entire business over a given period; and works out what share of that overall cost this one project should fairly bear, then extends it across the delay period. This formula’s strength is that it's grounded in the Contractor’s real accounts rather than a bid estimate, which makes it harder to dismiss as speculative. However, this formula requires the Contractor to maintain the accounts in reasonably good order to use it at all.

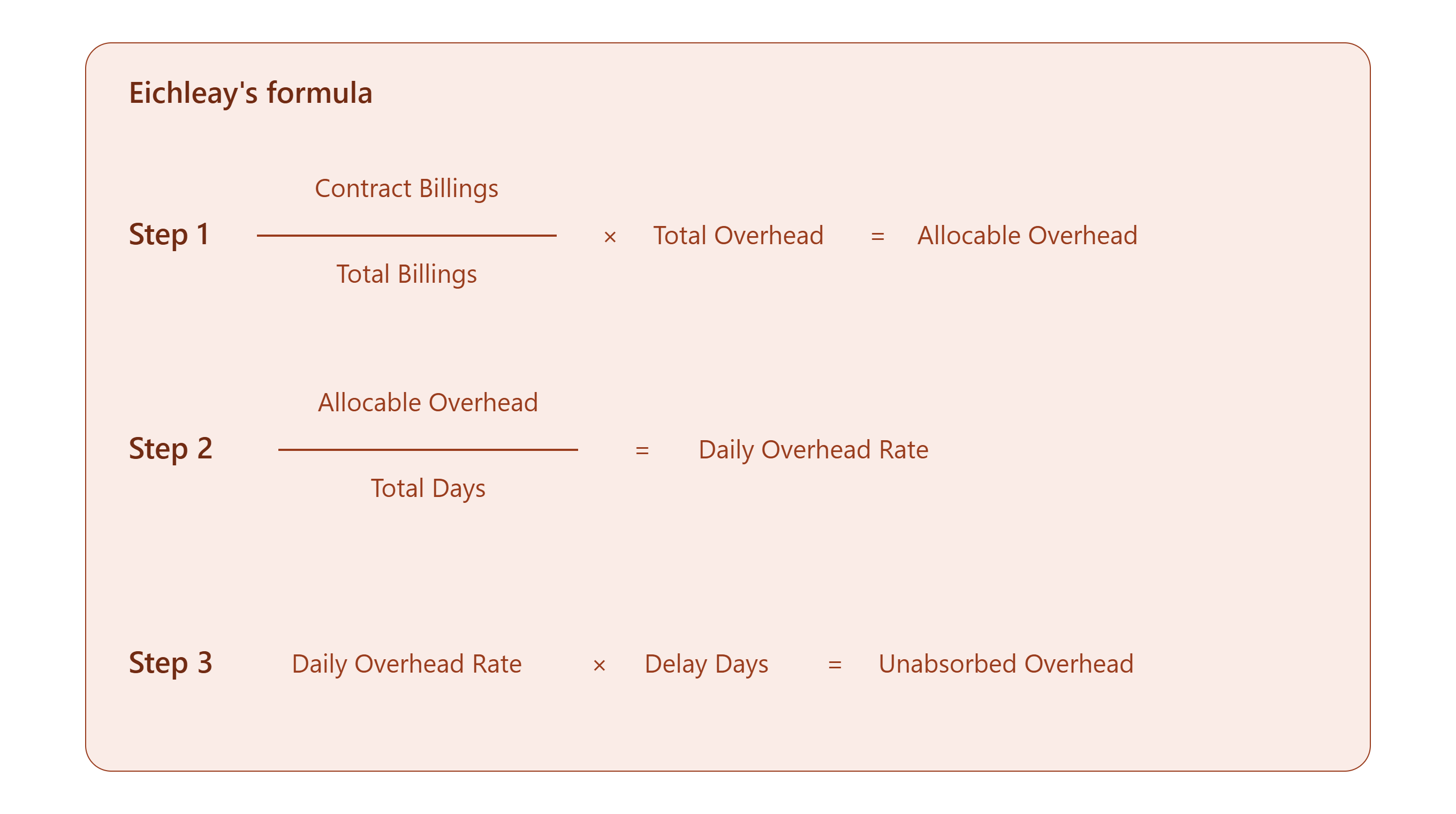

Eichleay's formula also starts from the Contractor’s actual company-wide figures, but it's built specifically around delay situations where a project comes to a near-total stop, i.e., where the Contractor’s resources were sitting idle, unable to be deployed elsewhere, for a defined stretch of time (i.e., suspension of work for no fault of the Contractor and standby to immediately restart the work by the Contractor). It ties the overhead recovery closely to the Contractor’s actual billing pattern during the real (not the originally planned) contract period. It tends to suit contracts where the project effectively froze rather than merely slowed down.

None of the three is automatically "correct". Which one suits a given claim depends on the kind of delay a Contractor faced, how the Contractor’s company keeps its accounts and what the contract allows. What matters, for now, is simply that there is a real, recoverable head of loss and there is more than one accepted way to put a number on it. In recent years, Indian courts have become stricter. The Courts now say that a contractor cannot just plug numbers into Emden’s or Hudson’s and win. The Contractor must also show a loss of opportunity, i.e., the Contractor has to prove that because this project was delayed, the Contractor had to turn down another specific contract where the Contractor could have utilized that head office staff.

The Hon’ble Supreme Court of India has issued a word of caution recently that these formulae deal with theoretical mathematical equations while being based on factual assumptions. Each of these formula is dependent on various assumptions, which, if not present, will not justify the use of the said formula. So Eichleay isn't treated as a formula that sidesteps the evidentiary burden but it has its own assumptions that must independently be proven. The Courts did note the Eichleay's Formula is more precise and accurate in calculating loss of profits since it requires the contractor to itemise and quantify the total fixed overheads during the contract period, but "more precise" means it demands its own rigorous documentation (itemised fixed overheads, contract-by-contract billing comparisons), not that it excuses the contractor from proof altogether.

The right one for your situation is a separate conversation.

Sample Project with Example

A road contract, value Rs. 200 crore, meant to be completed in 20 months. It actually took 30 months, i.e., a delay of 10 months, none of it attributable to the Contractor. The Contractor's tender had priced in 5% for head office overheads and 10% for profit.

Input data:

Input | Value |

Head office overhead % (as priced in tender) | 5% |

Profit % (as priced in tender) | 10% |

Combined overhead + profit % | 15% |

Contract sum | Rs. 200 crore |

Original contract period | 20 months |

Delay period | 10 months |

************************

Input data:

Input | Value |

Actual audited overhead + profit % (company-wide) | 12% |

Contract sum | Rs. 200 crore |

Original contract period | 20 months |

Delay period | 10 months |

*************************

Input data:

Input | Value |

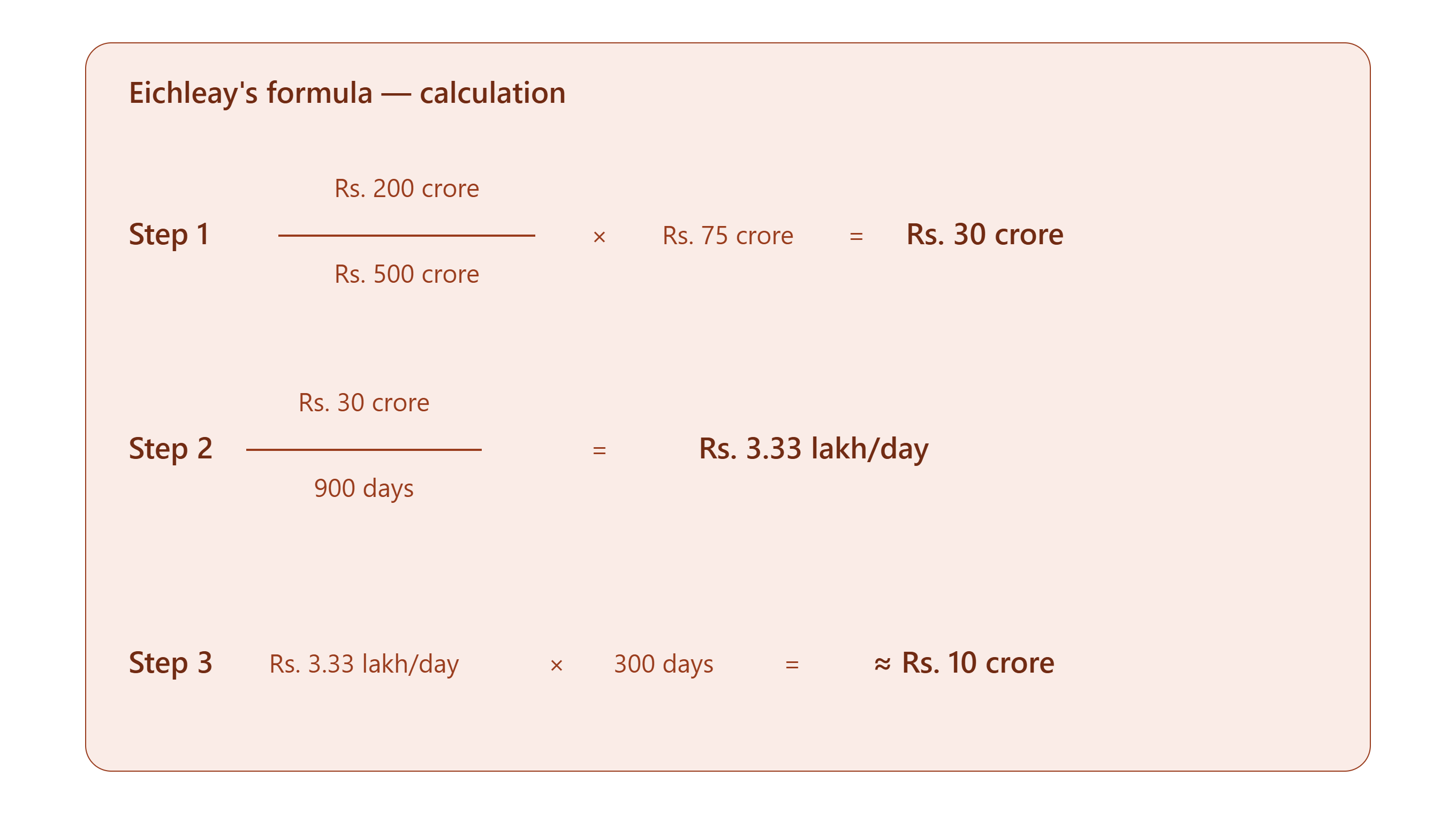

This contract's billings during the period | Rs. 200 crore |

Contractor's total company-wide billings during the period | Rs. 500 crore |

Contractor's total actual head office overhead expense for the period | Rs. 75 crore |

Actual (extended) contract period | 30 months = 900 days |

Delay period | 10 months = 300 days |

The Comparison

Formula | Basis of the percentage/figures used | Result |

Hudson's | Tender-priced percentage | Rs. 15 crore |

Emden's | Actual, audited company-wide percentage | Rs. 12 crore |

Eichleay's | Actual company-wide billings and overhead expenditure | Rs. 10 crore |

Same project. Same 10-month delay. But different result.

The decisions is which formula the Contractor's own paperwork can actually support, i.e., the tender workings, the audited accounts or the actual billing records; and whether the claim is being framed as overheads-and-profit together, or overheads alone with profit argued separately.

Ultimately, be prepared to support your case.